Understanding the difference between a financial advisor and a fiduciary is critical to your financial success. If you need a financial professional for advice, you need that advice to be right for you, given your circumstances and your goals.

You should be comfortable with who is giving you financial advice because your financial future is too important to leave to chance. You want to build wealth, secure a stable financial future, and make the most of your financial situation. You want to enjoy a life where money gives you the freedom to live as you desire.

Imagine having a trusted advisor by your side, guiding you towards financial success without any worry or uncertainty. Working with a fiduciary vs a financial advisor can empower you to make informed decisions and take control of your financial well-being.

Sadly, too many financial advisors do not provide sound advice; more importantly, they are not required to do so. This article will delve into the distinctions between a financial advisor vs a fiduciary, helping you make an informed decision about who to trust with your financial future.

Financial Advisor Defined

A financial advisor is sadly a very loose term. Almost anyone can claim to be a “financial advisor.” If that advisor works with regulated securities or insurance (stocks, bonds, mutual funds, annuities, or insurance policies), they typically have a license (see below) to offer their investment advice.

Financial advisors may offer financial planning services and investment management; they can work independently or as registered representatives of major brokerage firms and insurance companies. The usual services offered include:

- Retirement Planning – advisors may develop a short or long version of a plan to help their clients achieve specific goals.

- Investment Management – investment advisors, money managers, and wealth managers usually manages their clients’ investment accounts by recommending and often selling stocks, bonds, mutual funds, annuities, and other insurance products.

- Insurance Planning – advisors make recommendations about the type and amount of insurance their clients should have. Here again, many financial advisors sell these insurance products for a commission. Insurance recommendations are listed under insurance planning and investment planning because many financial advisors consider insurance policies to be both insurance and investment tools.

- Tax Planning – some financial planners and advisors can offer advice on how to lower their clients’ taxes.

- Estate Planning – financial advisors also often develop a plan for how to distribute assets after their client’s death and assist them with developing wills and trusts.

Fiduciary Defined

A fiduciary is a very specific term. Very few people qualify as a fiduciary because of the legal obligation to always act in the client’s best interests. There are several different types of fiduciaries, which include:

- Attorneys

- Trustees

- Conservators

- Legal Guardians

- Principals of a company

- Controlling shareholders

- Fiduciary Financial Advisors

For the purpose of this article, we’ll focus on the fiduciary financial advisor. This is a very unique group of financial advisors licensed by the Securities and Exchange Commission or state regulator.

Fiduciary financial advisors, such as a certified financial planner, provide their clients with advice and/or manage their client’s assets. While this is similar to the role of a regular financial advisor, the difference is that a fiduciary financial advisor must provide these services and manage these assets without any conflict of interest and solely in the client’s best interest.

That’s the key difference between a fiduciary financial advisor and a financial advisor.

The choice between financial planners vs fiduciaries will significantly impact the service and products they offer. How can you truly be sure you are being sold a financial products that can help you reach your goals?

Services Performed by Fiduciary Financial Advisors

The usual services offered include those offered by a regular financial advisor, but at a more detailed and rigorous level, along with several additional services:

Retirement Planning – fiduciaries develop more detailed plans to help their clients achieve specific goals.

Investment Management – fiduciaries manage their clients’ investment accounts by identifying specific targets and measuring performance against those targets. They do not sell any investment products and are required to act in the clients’ best interest.

Insurance Planning – fiduciaries analyze their client’s assets and liabilities, earnings, and cashflow to determine where there is risk exposure. Then, they recommend the appropriate type and amount of insurance to cover those risks. Fiduciaries will work with their clients to obtain the right insurance, but they will never compromise their objectivity by selling it for a commission.

Tax Planning – fiduciaries analyze their client’s entire current tax situation and determine whether and where significant tax relief is available. They then work with the client to position themselves to take advantage of those potential tax savings.

Estate Planning – fiduciaries develop detailed estate plans to minimize the impact of estate taxes, securely distribute assets to heirs and favored causes, and assist them with developing wills, trusts, and potentially more sophisticated techniques.

Legacy Planning and Management – fiduciaries often assist multiple generations to ensure that a family’s legacy passes between generations and is managed prudently to accomplish such multi-generational goals. To the extent that charitable giving is included in a client’s legacy goals, fiduciaries can assist in managing private foundations, donor-advised funds, and endowments.

Wealth Planning – fiduciaries often provide their clients with comprehensive wealth planning services, including all of the above. Working with a wealth management advisor is an all-encompassing approach.

When you receive advice from a fiduciary vs a financial advisor, you are getting genuinely objective information. The line between good financial advice and a sales pitch is blurred with a financial advisor who isn’t a fiduciary.

No one should grapple with the uncertainty of hidden charges and the real motivations behind financial advice. Working with a fiduciary financial advisor eliminates these worries with transparency from the start about their fee structure and compensation.

Fiduciary financial advisors are more inclined to offer bespoke and thorough financial planning because they are bound by their duty to prioritize the client’s best interests. This approach helps them to closely align with the client’s unique objectives, risk appetite, and financial circumstances.

Types Of Fiduciary Financial Advisors

Because of the comprehensive capabilities of a fiduciary financial advisor, it’s important to understand what type of fiduciary you might need.

Discretionary Fiduciary Advisor

A discretionary fiduciary advisor is given authority to exercise control over the client’s accounts. That control must be exercised in the client’s best interest, but the discretionary fiduciary advisor does not seek the client’s permission before making decisions. They report to the client regularly (typically quarterly to annually) on actions they have taken and the results, but the client is not involved in these daily decisions.

Discretionary authority is typically given over investment accounts, but in extreme situations, clients extend this authority to cover all their assets and liabilities.

Non-discretionary Fiduciary Advisor

A non-discretionary fiduciary advisor does not exercise control over accounts or assets. This type of fiduciary acts in a consultative manner, providing recommendations to the client and helping implement those recommendations. They always obtain the client’s approval beforehand.

Retirement Plan Fiduciary Advisor

This type of fiduciary serves a specific role focused exclusively on retirement plans employers provide for their employees. Because the assets in these plans belong to the employees but are being provided and/or managed by the employer, the employer has a fiduciary duty to act in the best interest of the employees. The IRS provides a more detailed list of responsibilities.

Many employers hire retirement plan fiduciaries to take on this responsibility. Many individual clients are also owners or key executives of companies offering their employees retirement plans requiring this type of fiduciary.

As you might expect, the definition of fiduciary encompasses several different roles. Attorneys, trustees, guardians, and conservators are all fiduciaries. As they provide their services, they must do so free from any conflict of interest, to the best of their abilities, and in the client’s best interest.

Fiduciary vs Financial Advisor Key Differences

As should be clear by now, the fiduciary – specifically, for this article, the fiduciary financial advisor – is held to a higher standard than a regular financial advisor. The debate over fiduciary vs financial advisor often focuses on the level of obligation each has to act in the best interest of their clients. Unfortunately, most are unaware of the differences in legal and ethical standards when comparing a fiduciary financial advisor vs a financial advisor.

This difference shows itself in the following key ways:

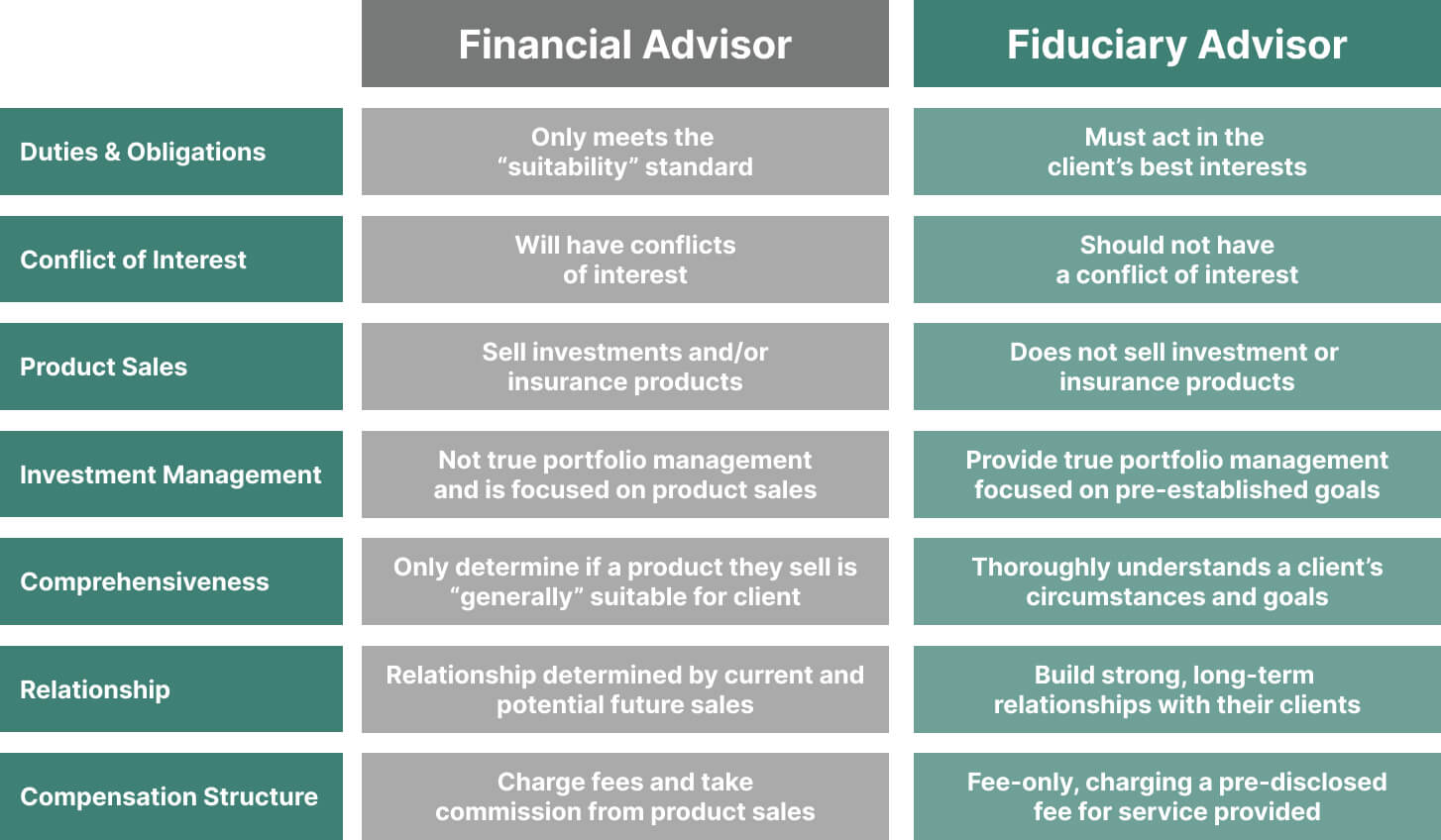

Duties and Obligations

A fiduciary must make recommendations and act in the client’s best interests.

A regular advisor only has to meet the “suitability” standard. Suitability means the advice or product being sold generally fits the client’s needs.

Conflicts of Interest

A fiduciary should not have any conflict of interest with their client. A regular advisor often has a conflict of interest with their clients.

Product Sales

Fiduciaries don’t sell investment or insurance products. Regular investment advisors do sell investment and insurance products. This means that regular advisors implicitly take an adversarial role to the client; they are “selling” (and are motivated to do so), and the client is “buying” (and must look out for his/her own interests).

Investment Management

Fiduciaries provide true portfolio management, focusing on achieving specific goals for the portfolio established beforehand. Regular advisors can manage in the sense that any salesperson “manages” their accounts, looking for ways to sell more financial products to the account.

Comprehensiveness

Fiduciaries must take steps to understand a client’s circumstances and goals thoroughly. Regular advisors only have to determine whether a product they sell is generally suitable for a client.

Relationship

Fiduciary financial advisor typically build strong long-term relationships with their clients. Regular financial advisors can be transactionally focused. The level of the relationship is determined by the sale at hand and potential future sales.

Compensation Structure

Fiduciaries are fee-only, charging a fully disclosed fee for the services provided. Regular advisors can charge fees and take commissions from product sales.

How To Tell if Your Financial Advisor Is Truly A Fiduciary

The good news is that it is relatively easy to determine if an advisor is a fiduciary advisor. Any of these methods work, but we recommend using them all to determine if someone is a fiduciary advisor vs financial advisor

First, ask them – you should know whether an advisor is willing to speak truthfully. We recommend using this list of questions to ask a financial advisor. If they are uncomfortable with answering these questions, that will tell you something about how they will approach future communications with you.

Second – ask them to sign a fiduciary oath. The old adage, “trust but verify,” applies here. If an advisor tells you they have fiduciary duties, they should not have any problem with putting that in writing. The Fiduciary Oath was put together by “The Committee For The Fiduciary Standard” to advocate for the fiduciary standard.

Third, check their registration – perhaps we’re being overly cautious, but we suggest you “trust, but verify… and then verify again.” If your advisor is a Registered Investment Advisor (RIA), they are held to a fiduciary standard and must disclose any potential conflicts of interest or regulatory sanctions against them. AdviserInfo is the official government financial industry regulatory authority website where you can search an advisor’s record.

If the investment advisor is a fiduciary, it will be abundantly clear here.

Picking the Right Fiduciary Financial Advisor

We at First Financial Consulting believe you should only use a fiduciary, fee-only advisor. Whether you need a little or a lot of advice on personal finance, whether you just need a one-time consultation or a long-term relationship, we believe you owe it to yourself to know that the advice you will receive is right for you – that the advice is more than just “suitable,” that it is absolutely in your best interest.

In working for your best interests, the Securities and Exchange Commission requires fiduciaries to have an implicit obligation to a “duty of care,” meaning they must exercise reasonable diligence and prudence. A fiduciary financial advisor is bound to a fiduciary duty and must take steps to understand your circumstances and goals thoroughly.

Some fiduciaries will be better at this than others. A good, experienced fiduciary, like First Financial Consulting, will start by asking questions. We don’t jump to financial or investment advice. We need to understand our clients to better serve them.

Those back-end issues flow out of a comprehensive conversation with you, the client. We start with foundational questions, which include:

- What are your specific financial goals – short-term, intermediate & long-term?

- When do you want to retire?

- What are your key assets and liabilities? What do they earn? What cashflow do they generate?

- How are they going to change?

- What are your living expenses now, and what will they be in retirement?

- What specific goals are appropriate for your investment strategies?

- What are the risks to your current situation, and are they being mitigated?

- What legacy or financial benefit do you want to leave, and to whom?

- What protections do you want to provide your heirs from taxes, financial malfeasance, or lawsuits?

- How often do you want to review your situation going forward?

- What other questions need to be asked in your specific situation?

As you can see, our list of foundational questions is extensive. They cover the client’s present situation, desired future, and the potential heirs or favored charities. They cover assets, liabilities, income, and expenses. They cover potential risks and intended or desired changes. We call these foundational because they provide the appropriate foundation on which fiduciary advice and recommendations can be provided.

Imagine what type of advice you would receive if someone did not understand all your goals, the composition of your current financial situation, the risks you face, or what type of legacy you want to leave. It is possible that if a sufficient number of these questions are asked, the fiduciary duty to care would be met, but it wouldn’t be the best advice.

Go Forth And Prosper

In conclusion, we return to the beginning. A fiduciary needs to do the best they can to achieve your goals. It is your interest which must be the north star. Ultimately, that means you are prospering. What that looks like for each client will be different because each client is different.

At First Financial Consulting, we take the time to learn what that means for you and then craft the plan and recommendations that will help you prosper. For most of our clients, that means we also help implement that plan to make sure nothing is lost or forsaken at that point. The best crafted financial plan is worthless if it’s not implemented and then monitored regularly.

There will be changes because life changes. Regular reviews of performance and the overall plan assure you that you can stay on track even in the face of the difficulties of life, the economy, and the markets.

If you’d like to begin a conversation about how we can help you, please use the button below to schedule a complimentary introductory appointment with a fee-only, fiduciary financial advisor.

Greg Welborn is a Principal at First Financial Consulting. He works with individuals and privately-owned businesses on financial planning issues including investment, retirement, and tax planning, among others.

Greg Welborn is a Principal at First Financial Consulting. He works with individuals and privately-owned businesses on financial planning issues including investment, retirement, and tax planning, among others.

FAQs | Fiduciary vs Financial Advisor

Fiduciary financial advisors, such as a certified financial planner, provide their clients with advice and/or manage their client’s assets. While this is similar to the role of a regular financial advisor, the difference is that a fiduciary financial advisor must provide these services and manage these assets without any conflict of interest and solely in the client’s best interest.

That’s the key difference between a fiduciary financial advisor and a financial advisor.

Using a government website like BrokerCheck is the official government financial industry regulatory authority website where you can search an advisor’s record. You can see any past or pending disclosures (regulatory event, arbitration, bond, etc) of any advisor or firm.

If the investment advisor is a fiduciary, it will be abundantly clear here.

Choosing a fiduciary over a non-fiduciary advisor offers several key benefits. Fiduciaries are legally obligated to act in your best interest, ensuring that their financial advice is unbiased and focused solely on your goals. This means they must avoid conflicts of interest and prioritize your financial well-being over their own profit.

This level of trust and commitment provides greater peace of mind, knowing that your advisor is dedicated to helping you achieve the best possible financial outcomes without any hidden agendas.

To determine if a financial advisor is a fiduciary, start by asking them directly, "Are you a fiduciary?" and request a clear, written confirmation. Inquire about how they are compensated—ask if they receive commissions from selling financial products or if they work solely on a fee basis.

Additionally, ask if they are willing to sign a fiduciary oath or agreement that outlines their obligation to act in your best interest.

Finally, ask about their professional designations, such as Certified Financial Planner (CFP) or Registered Investment Advisor (RIA), as these often indicate fiduciary responsibility.

We also have a long list of 20 questions to ask a financial advisor to learn more.